The return to Riyadh on 7 July of the second electronic World Cup, on an unprecedented scale, brought Saudi Arabia and the wider Middle East and North Africa (MENA) back to the forefront of the global game world. With the strong support of the World Cup for Electronic Competition and the Saudi Public Investment Fund, the total prize pool for 2025 will exceed $70 million and the competition project will cover 25 games.

The core electronic competition projects include Heroes Alliance, Dota 2, Anti-Terrorism Elite, EA Sports FC 25, Victory Top and Kings Glory. This year, new projects have been added, such as the Dauntless Compact, Chess.com (including the involvement of the King Magnus Carlson of the World), Crossing the Line of Fire and Mission Call: Black Action 6, and Fort Night, which was removed. The opening ceremony on 10 July will bring together heavyweight artists, such as Post Malone, DJ Alesso and cellist Tina Guo, to highlight the deep integration of the game with popular culture.

The cornerstone of Saudi game strategy and MENA market potential

The World Cup for Electronic Competition is a central pillar of Saudi Arabia ‘ s national game strategy. With the continued strong growth of the play industry in the MENA region through strategic investment and the natural development of indigenous play culture, the latest publication of the Middle East and North Africa Player Behaviour and Market Insight Report 2025 by the market research institute, Niko Partners, revealed key data for the region. Niko Partners has been tracking the markets of Saudi Arabia, the United Arab Emirates and Egypt (collectively MENA-3) over the past five years. These markets continue to expand, driven by increased player participation, increased disposable income and strong government interest in games and electric competition. MENA-3 presents great opportunities for enterprises that are able to grasp their cultural links.

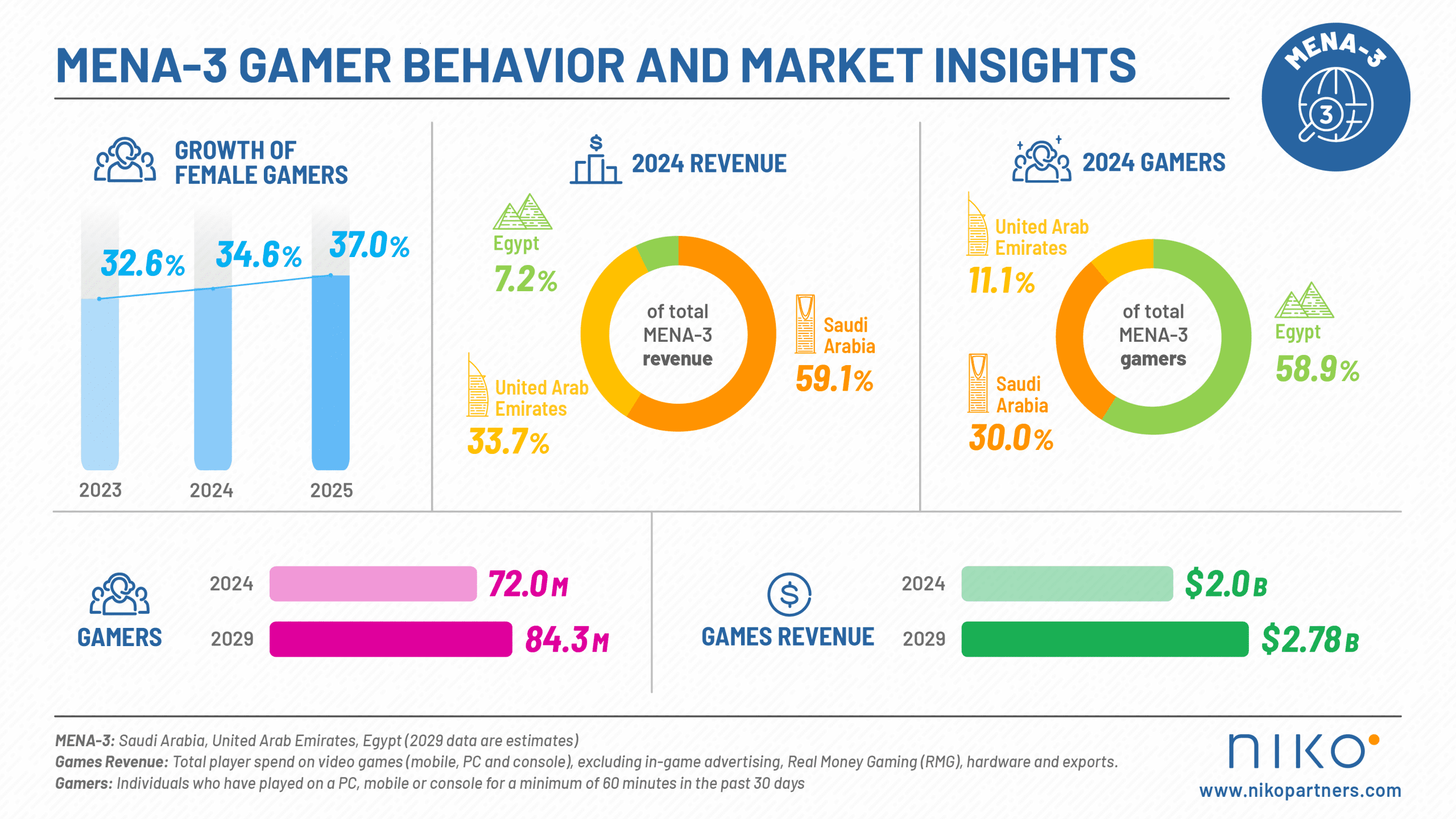

According to the MENA-3 market model of Niko Partners and five-year projections, the region ‘ s game revenues will reach $2 billion in 2024 (5.4 per cent over the same period) and are expected to grow to $2.2 billion in 2025. By 2029, market size is expected to reach $2.8 billion (6.8 per cent of the 2024-2029 compound annual growth rate of CAGR), and the expansion of the player base, the increase in average expenditure, the release of sub-generational hosts and the increase in localized inputs will be the main drivers.

MENA-3 market uniqueness

By the end of 2024, the total number of MENA-3 players had reached 72 million and was expected to grow to 84.3 million by 2029. Of these, the UAE has the highest value of $84.6; Saudi Arabia has the second highest value of $54.89; and Egypt has only $3.39.

MENA-3 is a unique region that has not traditionally been adequately served by global game companies. Arabic is the dominant language and localization requires a high degree of detail because of its right-to-left writing characteristics. The rejuvenation of players in the region is marked by the dominance of First Nations, with the vast majority of players under 35 years of age. The Governments of Saudi Arabia and the United Arab Emirates are investing heavily in video games and the electric competition industry as key areas for diversified economic growth in the coming years.

Player behaviour change

Niko Partners, based on a survey of 1580 players, revealed key changes in player demographics, behaviour and participation. The share of women players rose from 32.6 per cent in 2023 to over 37 per cent, reflecting the increased availability and inclusiveness of play ecosystems. Egyptian players are most active, with an average length of 11.8 hours per week on PC, mobile and mainframe platforms, higher than the average of 10.8 hours in the region. The participation of 54.6 per cent of MENA-3 players in some form (playing, watching or participating in competitions) indicates that a strong culture of competition is taking shape. In addition, 82.2 per cent of players were aware of the generated AI and more than half expressed interest in its applications in video games. The United Arab Emirates plays a leading role in this area (59.3 per cent).

Sports games dominate hosts/PCs, and fragmentation payments are key to ecological realization

According to data from the Niko Partners report, sports-like games dominate the MENA-3 area, particularly football-like games such as EA Reports FC and eFootball. On the PC platform, 33.4 per cent of players listed sports games as the most popular type of play. This percentage is higher than 44.1 per cent on the mainframe platform. On a mobile platform, sports games rank second after puzzle puzzles. Of the total participation in sports on all platforms, football plays contribute an impressive 70-80 per cent. It highlights the deep cultural roots and player preferences of football in the region.

Although the total length of time spent on sports games decreased in 2025, the average expenditure on players showed an increase. Among the five most popular game types played by players, sports players have the highest correlation with electric competitions (including participation, watching or playing). This trend coincides with the growing institutionalization of electric competition in the region, where regional events increasingly include football games.

Monetization of debris and payment ecosystems

Effective liquidity in the MENA-3 market is one of the core challenges, especially in North Africa and the Levant region. The issue was explored in depth in the White Paper entitled “The Analysis of Monetization Patterns of Video Games in the Middle East”, published jointly by Niko Partners and Xsolla: about 67 per cent of the population of the MENA region as a whole is in a state of “no bank account” or “insufficiency of banking services”. This means that traditional, credit card/debit card payment patterns are not sufficient to support large-scale monetization needs. However, the digital wallet solution is gaining increasing popularity, particularly in Egypt. For example, up to 74 per cent of Egyptian players use Vodafone Cash to buy inside.

Successful in the MENA-3 market, localization is not limited to the content of the game (linguistics, cultural approximation), but must cut across the entire chain of monetization strategies, payment modalities, platform selection, etc. Businesses need to be effectively localized at the cultural, linguistic and technical levels to better translate user participation into real income. The great event of the Saudi Electric World Cup, which brought together the growing market size of the MENA-3 region, the large group of young players, the deepening culture of electric competition and the strong support of the Government for industry, brought together the rapid rise of the Middle East and North Africa as an essential force in the global game map.