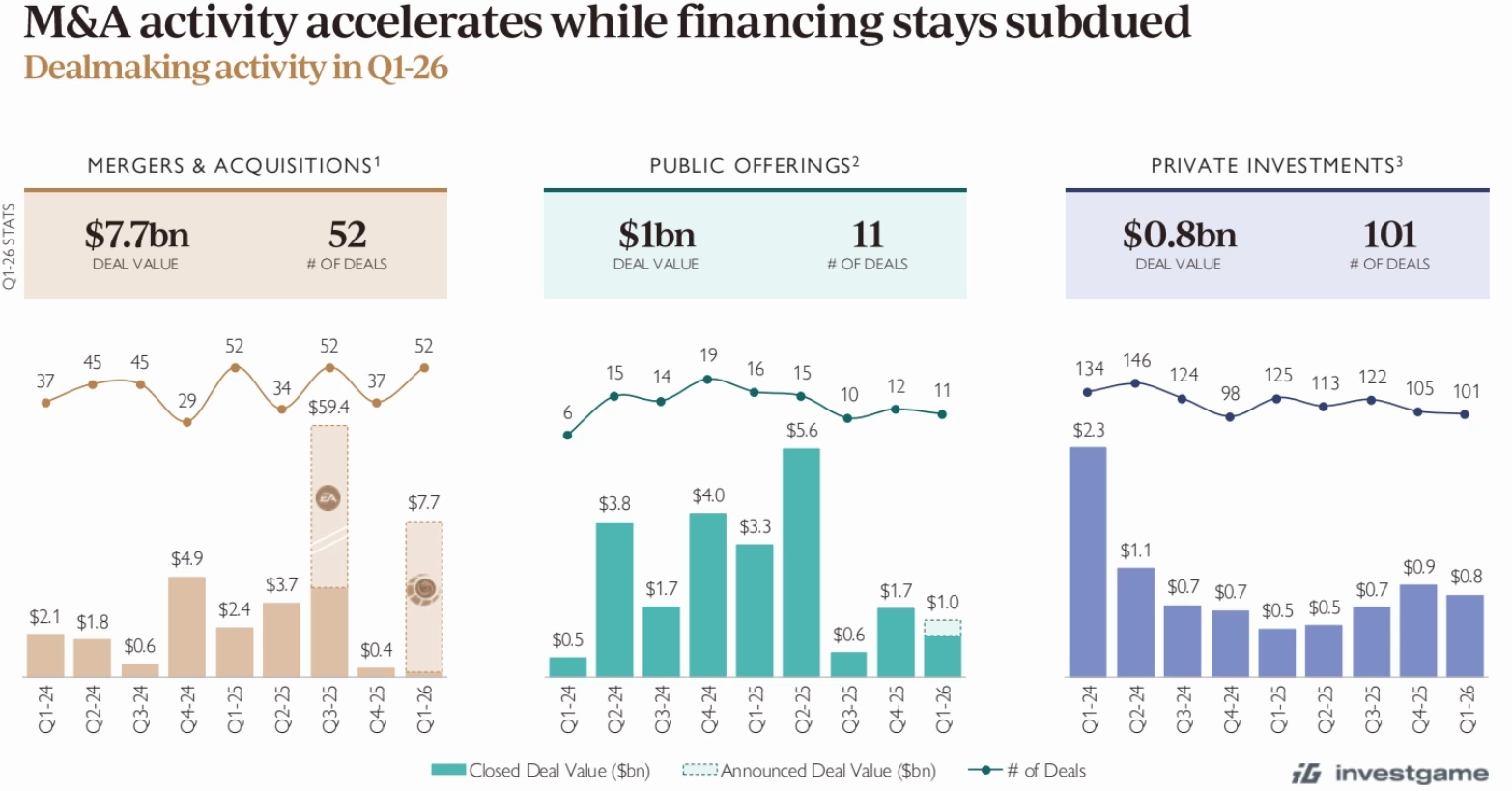

According to the 2026 Q1 video game market update published by Aream & Co, 52 mergers and acquisitions were completed in the game industry in the first quarter of 2026, with a total value of $7.7 billion. The first quarter of 2026 was the highest trade since the end of the epidemic, if “mega-transactions” such as Microsoft’s acquisition of the blizzard were excluded.

This figure is more than three times that of the first quarter of 2025 ($2.4 billion). This compares to only $400 million in the fourth quarter of 2025. In the first months of 2026, the mobile end dominated the M & As flow, with Savvy Gomes Group taking the bulk of the transactions. During the same quarter of Savvy’s $6 billion acquisition of pediatric technology, its subsidiary, Scopely, bought the Turkish super-recreational game company Loom Games at $1 billion. Other transactions in the mobile market include: the acquisition of 70 per cent of JustPlay’s shares by NCSoft for $202 million; the announcement by the United States and Thailand of plans to purchase Mattel163 at full cost for $159 million; and Nazara’s agreement to buy 50 per cent of Blueile’s social play platform for $100 million. Aream & Co reported that during the last quarter, the public collection unit remained low, with 11 transactions totalling $1 billion. Private investment grew over the same period but declined in the ring, with 101 transactions totalling $800 million.

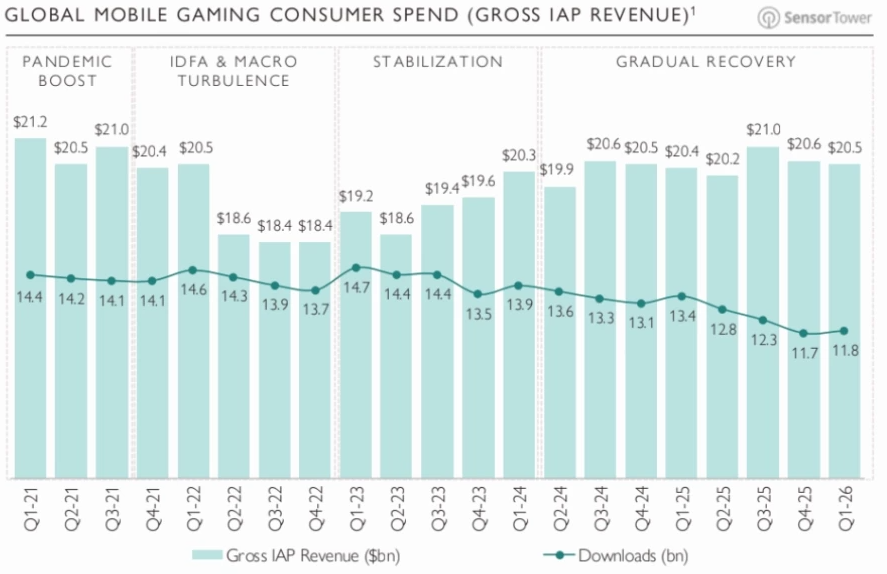

The report states: “The wider macroeconomic counterwind and AI-driven market rotations have placed overall pressure on open stock markets, and game units have fallen in tandem with wider software stock sales. As a result, open capital distribution remains low.” The number of early corporate risk investment-led transactions dropped to a low after the outbreak. Arcadia, Bitkraft Ventures and Griffin are the three most active institutions in this field. In addition to M&A activities, the report analyses the income performance of the various playing platforms. Steam and the mainframe, whose revenues exceeded those of the mobile end of the in-house purchase, received attention because of growth.

Steam’s quarterly revenues reached a record $5.6 billion, driven largely by Western game developers, and, thanks to the success of Switch 2, the host income reached a record $21.7 billion. Not only did it compensate for the decline in PS5 and Xbox sales, but it also exceeded the $20.5 billion applied in-house purchase income at the mobile end of the quarter. Despite the decline in downloads over time, the mobile end remained “stable” and income remained above $20 billion for seven consecutive quarters.

Loom James, Microfun and Century James were ranked among the fastest growing issuers in the United States, with the Bandai South Dream Palace and Vooodoo ranked fifth. The report notes that mobile play studios in Asia and Turkey continue to receive a growing share of income.